Alinity Wealth Management

Matthew P Kubicek

Partner|CFP®, CLU®, RICP®, CPWA®

Alinity Wealth Management

Get a financial plan that prioritizes your priorities.

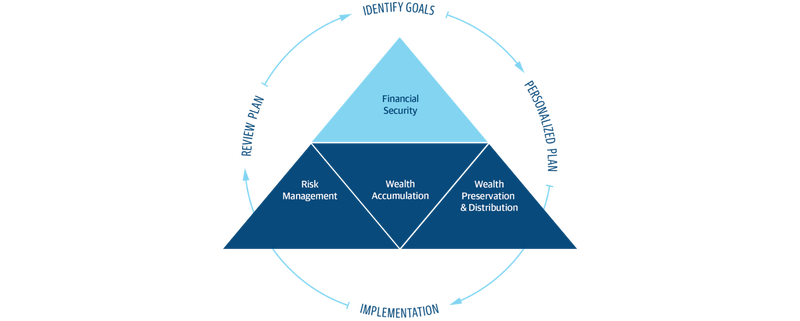

We will guide you through each step so you'll feel confident that you can do the things you've always wanted to—without having to worry if you can. See how we'll get it done below:

Look at where you are today

Your plan will help you make the most of what you already have, no matter where you're starting from, and give you a snapshot of your financial big picture.

Identify where you want to go

Whether it's shorter-term goals like managing your debt, or longer-term ones like saving for a new home, or retirement, your financial plan will show you how you're tracking, help you understand what's working, and point out any gaps you might have.

Put together range of options to get you there

Looking across all your goals, you'll get personalized recommendations and strategies to grow your wealth while making sure everything's protected. And I'll help you determine the right moves to make today and later on. Your financial plan is based on your priorities. As those priorities change throughout your life, we'll shift the financial strategies in your plan, too-so your plan stays flexible, and you stay on track to consistently meet goal after goal.

Investments

We believe you shouldn’t invest in any strategy or idea you can’t explain in plain language.

First and foremost, we believe investment decisions should always be guided by a comprehensive financial plan. It is crucial that your investment strategies align with the goals and objectives you have for your future!

In general, we believe short-term goals require greater safety and security of principal value since they will be used soon while long-term goals benefit from the opportunity for greater growth. Regardless of what specific investments we recommend, we always want that investment to be comfortable and understood by you and fully align with your other financial planning.

Investments of course are only one facet of your financial planning. It’s important to coordinate your investment strategy with your tax, insurance, and estate planning to build out a comprehensive and efficient wealth plan.

Tax-Efficient Strategies

When congress updates the tax code, they rarely simplify it. Instead, our taxes get more and more complicated throughout time, increasing our need for smart tax strategies. When we are young W2 employees, the questions are straight forward: Roth 401k or Pre-tax 401k? A quick run through of today’s tax rates compared to estimated future tax in retirement can bring a quick answer. However, as we grow in our careers and families, we ultimately earn more income, gain more assets, pay down more debt, establish more or larger businesses, inherit assets, and see our taxable income continue to glide skyward.

We don’t want you to pay any more in tax than you need to, so we look not only at today’s tax situation for you but look way down the road in your financial plan to see what things look like in retirement and for legacy. Then we make the best decisions possible today on how to position assets and income to pay the least in taxes over the course of our lifetime (and legacy), not just focusing on the next filed tax return. Once we have that strategy in hand, we coordinate with your CPA and tax preparer to review and implement.

Estate Planning

We’re pretty sure there is a 100% chance of dying, we just don’t know when that end date will occur. Our role is to help you identify and design what you want to occur should that day show up sooner than expected. For families, this means thinking through who raises our kids (guardianship/tutorship), who doles out the money for the kids (trustee of the trusts we would establish), and who is going to take care of the administration of these things at our death (executor/executrix).

For all of us, who gets our stuff when we die? Not just the 401k and house, but Great Aunt Edna’s jewelry or the family land too. Who inherits the business: both kids or just the one who is involved in it? How can we make sure they both inherit an equal value though if just one gets the whole business value? Who takes care of things if I’m still living, but need help with administration or decision making?

These are just a few of the many questions in our estate planning that need answers. And that’s where we come in to assist with that design process, figuring out what you truly want to happen. We’ll coordinate with your attorney or help you find one to draft it all up so that what you want to occur, will occur.

Insurance

We solve risk-based needs first. This means that if you don’t have proper health insurance, or emergency funds, or enough life insurance to provide for your family if you don’t wake up tomorrow, we solve that problem first. It makes very little sense to implement a great investment strategy if there is a lurking risk that can blow up your entire financial security.

For us, that means we take a comprehensive analysis of all risks that could befall a client: the risk of dying too soon, living long, encountering a sickness or injury and being unable to work, liability coverages for home and auto and umbrella policies, identity theft, or business liability. There are many mines hidden along the road of life and we want to make sure we are out ahead clearing the way of those perils.